Understanding the Taxation of Cryptocurrency Transactions

Article Highlights:

- How Cryptocurrency is Treated for Tax Purposes

- Capital Asset

- Who Keeps Track of Cryptocurrency Ownership and Transactions

- How Many Cryptocurrencies Are There?

- What Is Cryptocurrency Mining?

- What Is a Cryptocurrency “Hard Fork”?

- Why Is Cryptocurrency Appealing to Some?

- How Is the Value of Cryptocurrency Determined?

- Are Cryptocurrencies Good Investments?

- Virtual Currency and 1031 Exchanges

- First In—First Out (FIFO)

- Foreign Currency Transactions

- Foreign Bank and Financial Account (FBAR) Reporting

- Payments To Employees

- Payments To Independent Contractors

- Backup Withholding

- Charitable Donations of Cryptocurrency

- IRS Compliance Campaign

If you have purchased, owned, sold, gifted, made purchases with, or used cryptocurrency in business transactions, there are specific tax issues you need to understand. Unfortunately, the IRS has some unanswered questions and little specific guidance other than in Notice 2014-21 and Revenue Ruling 2019-24. This article includes the guidance from the Notice as well as general tax principles that apply.

One of the significant issues of cryptocurrency is how it is viewed for tax purposes. The IRS says that cryptocurrency should be treated as property. Every time it is traded, sold, or used as money in a transaction, it is treated much the same way as a stock transaction would be. This means the gain or loss over the amount of its original purchase cost must be determined and reported on the owner’s income tax return. That treatment applies for each transaction every time cryptocurrency is sold or used as money in a transaction, resulting in a major bookkeeping task for those that use cryptocurrency frequently.

Example: A taxpayer buys Bitcoin (BTC) to make online purchases without the need for a credit card. He buys a partial BTC for $2,425 and later uses it to buy goods worth $2,500 (let’s say the partial BTC was trading at $2,500 when he purchased the goods). He has a $75 ($2,500 – $2,425) reportable capital gain. This is the same result that would have occurred if he had sold the BTC at the time of the purchase and used cash to purchase the goods. This example points to the complicated record-keeping requirement for tracking BTC’s basis. Since this transaction was personal in nature, no loss would be allowed if the value of BTC had been less than $2,425 at the time the taxpayer purchased the goods. Of course, if the taxpayer in this example only sold a fraction of his Bitcoin – say enough to cover a $500 purchase – the gain would only be $15: $500/$2500 = .2 x 2425 = 485; 500 – 485 = 15.

On the bright side, cryptocurrency is generally treated as a capital asset for most individuals, so any gain is a capital gain. Any gain will be taxed at the more favorable long-term capital gains rates if the asset is held for more than a year. If the cryptocurrency is held as an investment and the sale results in a loss, the loss may be deductible. Capital losses first offset capital gains during the year, and if a loss remains, taxpayers are allowed a $3,000-per-year loss deduction against other income, with a carryover to the succeeding year(s) if the net loss exceeds $3,000.

If you don’t understand how cryptocurrencies function, here is a brief explanation.

Who Keeps Track of Cryptocurrency Ownership and Transactions?

Blockchain is a system of recording information in a way that makes it difficult or impossible to change, hack, or cheat the system and provides seamless peer-to-peer transactions around the world. A blockchain is essentially a digital ledger of duplicated transactions and distributed across the entire network of computer systems on the blockchain. Those who maintain these digital ledgers are referred to as miners.

How Many Cryptocurrencies Are There?

There are currently over 10,000 different cryptocurrencies traded publicly. The total value of all cryptocurrencies in mid-July 2021 was approximately $1.4 trillion. This was down from an April 2021 high of $2.2 trillion. This is evidence of the volatility of cryptocurrency.

What Is Cryptocurrency Mining?

Mining is how new blocks of cryptocurrency are inserted into circulation and how the network confirms new transactions. Mining is a critical component of the maintenance and development of the blockchain ledger. It requires sophisticated hardware that solves extremely complex math problems. The computer that finds the solution to the problem is awarded the next block (files where data about the cryptocurrency network are permanently recorded), and the process begins again. Miners are rewarded for their efforts in cryptocurrency.

For tax purposes, the IRS, in their guidance, have determined that miners are operating a trade or business. The value of the cryptocurrency earned (determined in U.S. dollars at the time of the transaction) is included in the gross income of that business. The business’ profit is treated the same as it is for any other business – taxed as ordinary income and subject to self-employment tax.

Example: An individual mines one Bitcoin in 2020. On the day it was mined, the market price of a Bitcoin was $10,000. The miner has $10,000 of business income in 2020, subject to income tax and self-employment tax. Going forward, the basis in that Bitcoin is $10,000. If the miner later sells it for $12,000, there is a taxable capital gain of $2,000 ($12,000 − $10,000).

What Is a Cryptocurrency “Hard Fork”?

You may have heard the term “hard fork” associated with cryptocurrency and wonder what it means. A hard fork occurs when there is a split in a cryptocurrency’s blockchain. Bitcoin had a hard fork in its blockchain on August 1, 2017, dividing into two separate coins: Bitcoin and Bitcoin Cash. Each holder of a Bitcoin unit was entitled to one Bitcoin Cash unit. Similarly, Litecoin, the fifth-largest cryptocurrency, had a hard fork, Litecoin Cash, in February 2018

.

In October 2019, the IRS released cryptocurrency guidance (Revenue Ruling 2019-24) that explains that a taxpayer:

- Does not have gross income from a hard fork of the taxpayer’s cryptocurrency if the taxpayer does not receive units of a new cryptocurrency; and

- Has ordinary income as a result of an airdrop of a new cryptocurrency following a hard fork if the taxpayer receives units of the new cryptocurrency. (An airdrop is a distribution of cryptocurrency to multiple taxpayers’ distributed ledger addresses.)

According to the IRS, taxpayers who received Bitcoin Cash as a result of the 8/1/2017 Bitcoin hard fork received ordinary income because the taxpayers had an “accession to wealth.” Further, the date of receipt and fair market value to be included in income depended on when the taxpayer obtained dominion and control over the Bitcoin Cash.

Why Is Cryptocurrency Appealing to Some?

Cryptocurrencies appeal to their supporters for a variety of reasons.

- Supporters see cryptocurrencies such as Bitcoin as the future currency. They are racing to buy them now, presumably before they become more valuable.

- Some supporters like the fact that cryptocurrency removes central banks from managing the money supply since these banks tend to reduce the value of money via inflation over time.

- Other supporters like the technology behind cryptocurrencies, the blockchain, because it’s a decentralized processing and recording system and can be more secure than traditional payment systems.

- Some speculators like cryptocurrencies because they’re going up in value and have no interest in the currencies’ long-term acceptance as a way to move money.

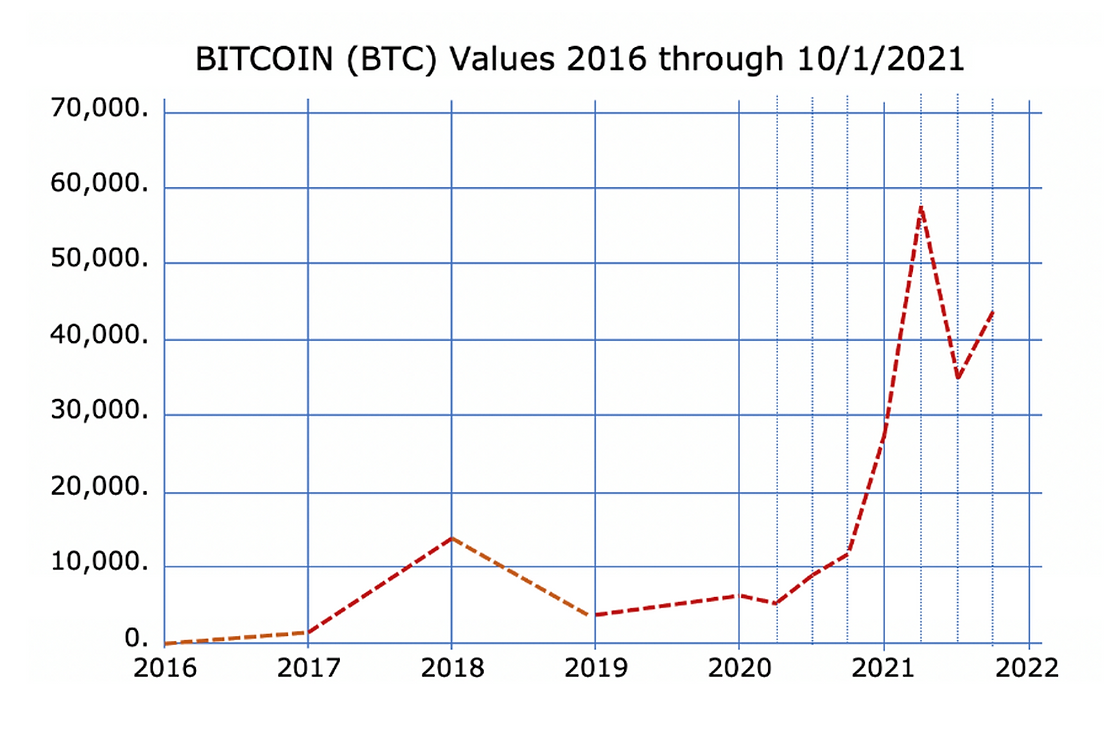

How Is the Value of Cryptocurrency Determined?

Unlike corporate stocks, whose values are based on current earnings and the potential for growth, cryptocurrency values are based on what a willing buyer is willing to pay a willing selling. Using Bitcoin as an example, you can see the volatility associated with this most popular cryptocurrency.

Are Cryptocurrencies Good Investments?

That depends upon whom you talk to. Some cryptocurrency investors have made substantial amounts with their investments, while others have lost substantial amounts. Cryptocurrencies may go up in value, but many investors see them as mere speculations, not real investments. Just like real currencies, cryptocurrencies generate no cash flow, so for you to profit, someone must pay more for the currency than you did.

Contrast that to a well-managed business, which increases its value over time by growing the profitability and cash flow of the operation. Some notable voices in the investment community have advised would-be investors to steer clear of cryptocurrencies. Warren Buffett once compared Bitcoin to paper checks: “It’s a very effective way of transmitting money, and you can do it anonymously and all that. A check is a way of transmitting money too. Are checks worth a whole lot of money? Just because they can transmit money?”

Here is some guidance that applies to specific issues:

Virtual Currency and 1031 Exchanges

Many virtual currency investors believe they can exchange one type of virtual currency for another without any tax consequences. Unfortunately, that is not true. Beginning in 2018, Congress altered the rules related to exchanges, limiting them to real estate transactions. Thus, investors in virtual currency who trade one type of virtual currency for another will have to treat exchanges as a sale and purchase and are required to report their capital gain or loss for each exchange.

First In—First Out (FIFO)

When trading stocks, investors who purchase various stock lots at different times and for different costs can choose which stocks they are selling for a specific transaction, allowing them to minimize their taxable gains. Brokerage firms generally can identify blocks of stock. This does not seem to be the case for cryptocurrencies, and the IRS has not provided any guidance. Thus, it would seem cryptocurrencies would be traded FIFO.

Foreign Currency Transactions

Under currently applicable law, cryptocurrency is not treated as currency that could generate foreign currency gain or loss for U.S. federal tax purposes.

Foreign Bank and Financial Account (FBAR) Reporting

The Treasury Department’s Financial Crimes Enforcement Network (FinCEN) requires reporting certain foreign bank and financial accounts. The FBAR report is filed with that agency rather than the IRS. Through the filings for 2020, cryptocurrency transactions have not been required to be reported on the FBAR. However, in January 2021, FinCEN said that it intends to amend the regulations implementing the Bank Secrecy Act regarding FBARs to include virtual currency as a type of reportable account. No further details have been announced so far.

Payments To Employees

When cryptocurrency is used as payment to an employee, the usual payroll withholding and reporting rules still apply, and the employee must be issued a W-2. All amounts are reported in U.S. dollars.

Payments To Independent Contractors

Suppose independent contractors are compensated with cryptocurrency more than the equivalent of U.S. $600 (as determined on the payment date). In that case, the payment must be reported to the government by filing form 1099-NEC. Payments, whether more than $600 or not, are included in the independent contractor’s business income, and profits are subject to income tax and self-employment income tax.

Backup Withholding

There are situations when the payer is required to withhold payments to individuals who are not paying their taxes. In these cases, the IRS will notify the payer that they must withhold from payments to specific individuals and remit the withholding to the IRS. When payments to these individuals are made in cryptocurrency, the equivalent U.S. dollar amount of cryptocurrency payment and withholding must be determined when the payment was made to the individual. The withholding must be determined and remitted to the IRS in U.S. dollars. The current backup withholding rate is 24 percent of the payment.

Charitable Donations of Cryptocurrency

Instead of selling the cryptocurrency and donating the after-tax proceeds, a taxpayer can donate it directly to a charity. If the virtual currency has been held longer than one year, this approach provides significant tax benefits:

- The tax deduction will be equal to the fair market value of the donated cryptocurrency (as determined by a qualified appraisal), and the donor will not pay tax on the gain.

- This also results in a more significant donation because, instead of paying capital gains taxes, the charity will receive the full value of the donation.

IRS Compliance Campaign

The IRS has been engaged in a virtual cryptocurrency compliance campaign to address tax noncompliance related to virtual currency use through outreach and examinations of taxpayers. They plan to remain actively involved in addressing non-compliance related to virtual currency transactions through various efforts, ranging from taxpayer education to audits and criminal investigations. Taxpayers who do not properly report the income tax consequences of virtual currency transactions are liable for the tax, penalties, and interest. In some cases, taxpayers could be subject to criminal prosecution.

To further the IRS’ efforts to flush out taxpayers who may have cryptocurrency reporting requirements, a Yes/No question has been included on Form 1040 asking taxpayers whether they received, sold, exchanged, or otherwise disposed of any financial interest in any virtual currency during the tax year. When signing their return, a taxpayer attests under penalties of perjury to have a “true, correct and complete” return. Taxpayers who answered the cryptocurrency question “no,” and the IRS finds that they had reportable virtual currency transactions, could be subject to significant penalties.

If you have questions related to your involvement with cryptocurrency, please give this office a call.

Leave a Reply

You must be logged in to post a comment.